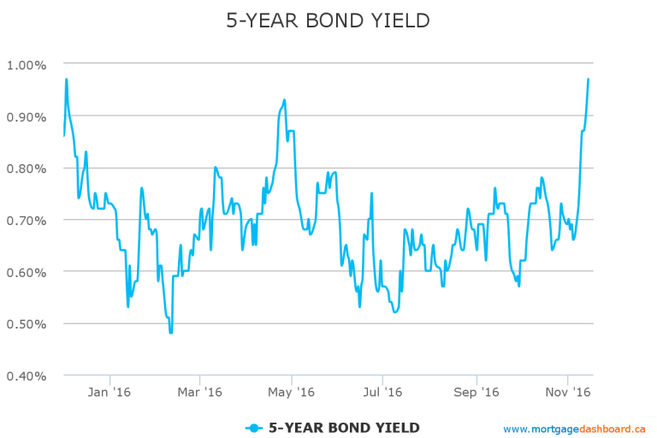

Donald Trump has “blown up” the bond market. That’s CNBC’s depiction after the president elect’s victory wiped out $1+ trillion of its value in the last week. Trumponomics, Trumpflation, the Trump Thump, Trumpulus, or whatever you want to call it, has incited fear in bondland. Traders envision 4%+ GDP growth, inflation, massive deficits, a potential U.S. credit rating downgrade and unravelling of the greatest bond bull market of all time. All of this is conspiring to reshape investors’ mindsets…radically. It’s raising the implied odds that 2016’s bottom in rates won’t be broken for several quarters, at a minimum. And if the bond market is somehow mispricing Canada’s economics prospects—and yields do fall 55+ bps to new lows—imagine what hideous fate that would portend for Canada. It’s a fate that, given a soon-to-be-robust U.S. economy (the destination for 73% of our exports), now seems Less probable But make no mistake, we’re staring at much uncertainty through 2018, not the least of which is:

But here’s something we can tell clients with confidence. The rate paradigm as we knew it on November 7th was transformed on November 8th. In 2017, the economy that we sell three-quarters of our goods and services to will be firing on two more cylinders, and net net, that could help Canadian business, boost Canadian inflation and be rate bullish. And if we’re wrong, borrowers will have far bigger problems to contemplate than not picking the bottom in interest rates.

0 Comments

Leave a Reply. |

Sylvie Ann Messer

|

RSS Feed

RSS Feed